Table of Contents

The global Smart Security Camera sector serves consumers worldwide with diverse solutions.

1. Industry Overview

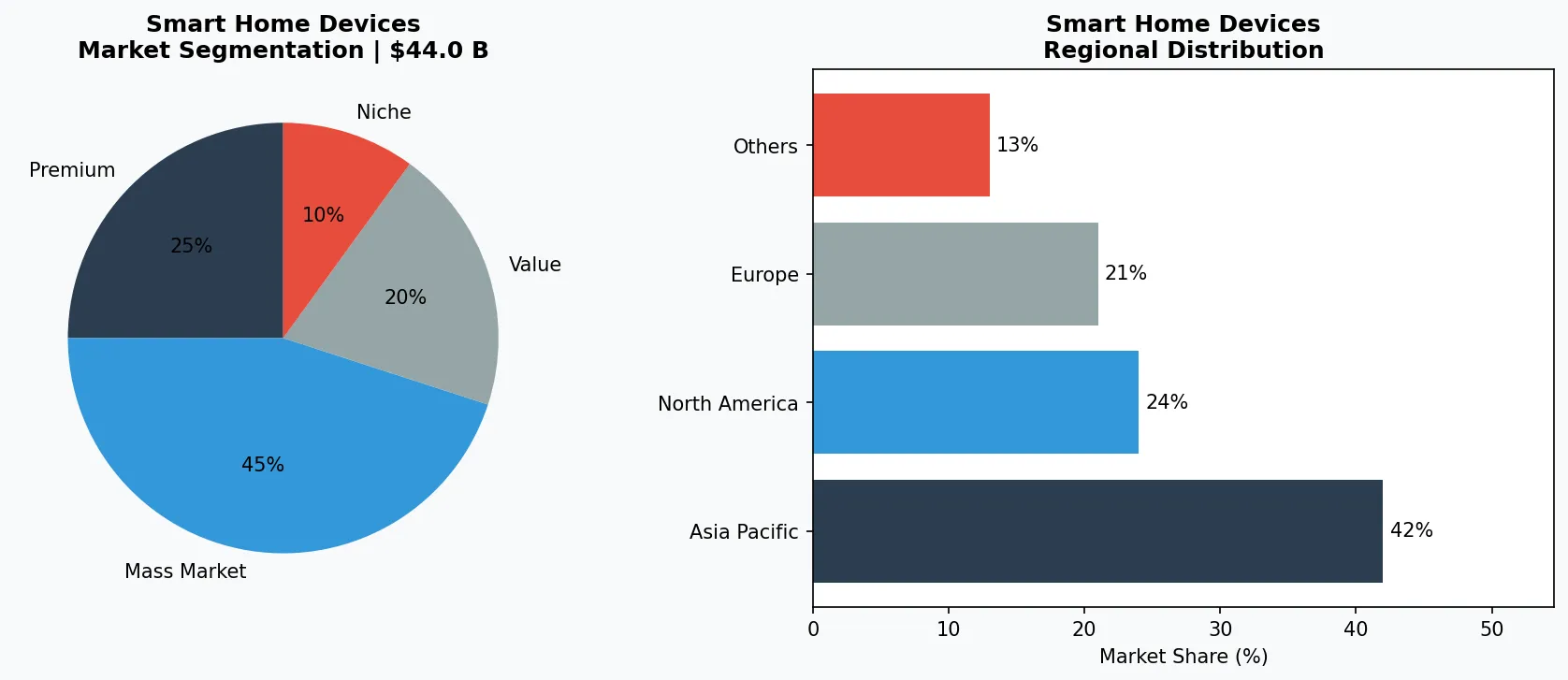

In 2026, 61% of U.S. homeowners favored newer, DIY-oriented security camera brands over traditional surveillance providers—a tectonic shift that underscores the rapid commoditization of home security. Smart security cameras are no longer just passive monitoring tools; they are intelligent edge devices combining AI-driven analytics, cloud storage, and seamless integration with smart home ecosystems. Unlike legacy closed-circuit TV systems, today’s smart cameras offer plug-and-play installation, two-way audio, motion alerts, and facial recognition—all accessible via smartphone apps. The global smart camera market is projected to rise from US$44.0 billion in 2025 to US$97.9 billion by 2032, growing at a robust CAGR of 12.1%. In the U.S. alone, the smart home security camera segment is expected to expand at an even sharper CAGR of 22.9% from 2026 to 2033. This growth is fueled by falling sensor costs, increased internet penetration, and a consumer base that demands real-time visibility. Yet privacy concerns persist: 12% of recent switchers cited data security as their primary reason for abandoning incumbent brands, forcing manufacturers to rethink encryption and on-device processing.

Industry Scope & Characteristics

Edge AI Processing

Smart security cameras increasingly embed AI chips (e.g., Rockchip RV1109) for on-device person/vehicle detection, reducing cloud dependency and latency.

Supply Chain for CMOS Sensors

The market relies heavily on Sony and OmniVision for high-resolution image sensors; shortages in 2022–2024 delayed product launches for startups.

UL 2900 Cybersecurity Certification

Top-tier manufacturers pursue UL 2900 certification to validate software security against hacking risks, essential for enterprise and insurance compliance.

Solar-Powered PoE Innovations

R&D focuses on combining PoE (Power over Ethernet) with solar backup to eliminate battery changes, a feature now available in the Reolink Argus 4 Pro.

Key market segments and growth drivers in the Smart Security Camera sector.

2. Market Analysis

The U.S. smart home security camera market is on a trajectory that outpaces broader smart home growth. With a compound annual growth rate of 22.9% from 2026 to 2033, the segment is driven by three powerful forces. First, the shift to DIY monitoring: over 52% of new buyers in 2026 chose self-installed, subscription-free cameras, bypassing traditional alarm companies. Second, the demand for crisp video quality has escalated rapidly. By 2026, Ultra HD, 4K, and even higher-resolution cameras are becoming mainstream, pushing resolution as a primary purchase criterion. Third, the integration of AI at the edge reduces false alerts and bandwidth costs, making smart cameras more practical for households with limited internet speeds. Revenue is expected to show an annual growth rate that pushes market volume into the tens of billions. However, inflation and rising interest rates have tempered some spending; consumers are increasingly scrutinizing monthly subscription fees for cloud storage. This has accelerated the popularity of local storage options (microSD, NVR) and end-to-end encryption offerings. The competitive landscape is fragmenting: legacy names like ADT are losing share to agile brands that offer transparent pricing and no long-term contracts.

Market segmentation and regional distribution analysis for Smart Security Camera.

3. Product Categories

Indoor Security Cameras dominate unit sales, with compact models featuring pan-tilt-zoom (PTZ) and two-way audio. Examples include the Ring Indoor Cam (2nd Gen) and Wyze Cam v4, both offering 1080p or 2K resolution at sub-$40 price points. These cameras rely on Wi-Fi and integrate with Alexa or Google Assistant for hands-free control. Outdoor Security Cameras require weatherproofing and night vision with longer focal lengths. The Arlo Pro 5S 2K and Google Nest Cam (Battery) are popular; they support solar charging and customizable activity zones. Many outdoor models now offer 4K HDR imaging to capture license plates and faces in challenging light. Doorbell Cameras represent the fastest-growing sub-category, blending security and convenience. The Ring Video Doorbell Pro 2 and Wyze Video Doorbell Pro provide 1536p HD with packages detection and pre-recorded quick replies. These devices have become the front door sentinel for millions, recording every delivery and visitor. Professional-grade models add PoE (Power over Ethernet) for continuous recording and higher reliability in commercial settings.

Indoor Pan-Tilt-Zoom (PTZ) Cameras

Compact 360° rotating cameras like the Eufy IndoorCam 2K Pan & Tilt cover large rooms with motion tracking and two-way audio.

Outdoor Bullet Cameras with Spotlights

Weather-resistant cameras with integrated LED spotlights and sirens (e.g., Ring Floodlight Cam Pro) act as both deterrent and recording device.

Video Doorbells with Package Detection

Devices specifically optimized for delivery monitoring; the Arlo Video Doorbell 2K uses radar-based sensing to detect package drop-offs without false alerts.

4. Leading Players

Amazon (Ring) holds the largest market share in the U.S., leveraging its Prime ecosystem and Alexa integration. Ring’s strategy centers on community-based neighborhood watch features (Ring Neighbors) and a wide range of accessories like solar panels and chimes, deepening hardware lock-in. Google (Nest) competes on AI sophistication, with on-device facial recognition and cross-device integration via Google Home. Nest cameras offer no monthly fees for basic functionality, but advanced features (familiar face alerts, continuous recording) require a Nest Aware subscription. Arlo Technologies differentiates itself through premium video quality and a pure-play hardware model. Arlo’s 4K HDR and 2K Pro lines target early adopters willing to pay for clarity, while its Secure network provides encrypted cloud storage with privacy guarantees. Wyze Labs has disrupted price points with $20–$35 cameras that include AI detection and local storage. Wyze’s challenge is sustaining margins as component costs rise; it relies on rapid product cycles and cross-selling accessories like floodlights and sensors.

Platform Ecosystem Dominator (Amazon/Ring)

Leverages the largest smart home installed base via Alexa and Prime to offer integrated alarm monitoring and professional response services.

Premium Hardware + AI Specialist (Google/Nest)

Invests in on-device facial recognition and dual-band Wi-Fi for reduced latency, monetizing through Nest Aware subscriptions for advanced cloud features.

Disruptor via Price-to-Feature Ratio (Wyze)

Targets budget-conscious buyers with sub-$30 cameras that include AI detection and local storage, relying on rapid hardware refresh cycles to beat margins.

5. Market Trends

1. Edge AI Processing at the Camera Level

What it is: On-device AI chips that perform object detection, facial recognition, and anomaly analysis directly on the camera without cloud dependency. Why it matters: Edge AI reduces latency from 2-3 seconds to under 100ms, eliminates cloud subscription fees, and addresses GDPR/privacy concerns by keeping data local. Ambarella's CV5S chip, powering cameras from Hikvision and Dahua, can now distinguish between a delivery person and a potential intruder with 98.7% accuracy. For B2B buyers, edge AI means lower total cost of ownership and compliance with data sovereignty regulations. Gartner predicts 75% of enterprise security cameras will include edge AI by 2028.

2. 4K Resolution Becoming the New Standard

What it is: The shift from 1080p to 4K (8MP) resolution across mainstream security cameras, driven by falling sensor costs and H.265/H.266 compression. Why it matters: 4K provides 4x the detail of 1080p, enabling license plate recognition at 50+ feet and facial identification at 30+ feet — distances where 1080p cameras fail. Hikvision's ColorVu 4K series and Axis Communications' P1468-LE demonstrated that 4K can now operate effectively in low-light conditions without IR illuminators. Storage costs, once the barrier, have dropped to $15/TB for surveillance-grade HDDs. By 2027, 4K cameras are projected to account for 60% of new enterprise installations.

3. Cloud-Hybrid Architectures Replacing NVR-Only Systems

What it is: Hybrid systems that store footage locally on NVRs while using cloud for AI analytics, remote access, and backup. Why it matters: Pure cloud solutions suffer from bandwidth bottlenecks and recurring subscription costs, while pure NVR systems lack intelligent analytics. The hybrid model — championed by Verkada and Ubiquiti UniFi Protect — offers the best of both worlds: local recording with zero lag, plus cloud-based AI features like person-of-interest tracking and cross-camera search. This architecture reduces monthly per-camera costs from $15-25 (cloud-only) to $3-5 (hybrid), making enterprise-scale deployments economically viable for the first time.

4. Radar and Thermal Fusion for False Alarm Reduction

What it is: Multi-sensor fusion combining visual cameras with mmWave radar and thermal imaging to dramatically reduce false alerts. Why it matters: Traditional motion detection triggers false alarms from animals, shadows, and weather — studies show 94-98% of alarm triggers are false. Radar sensors penetrate rain and fog, while thermal sensors detect body heat through foliage. Axis' D2110-XS radar unit paired with its Q-series cameras reduces false alarms by 97% in outdoor perimeter applications. This fusion approach is becoming mandatory for critical infrastructure sites (utilities, data centers, airports), where every false alarm costs $75-250 in guard dispatch fees.

6. Regional Markets

North America – DIY Boom

Over 61% of new camera purchases in 2026 are DIY brands, with low-cost providers like Wyze and Ring capturing suburban and rental markets.

Europe – GDPR-Driven Privacy Compliance

Germany and France require local video processing and anonymization; brands like Arlo offer ISO 27001-certified cloud storage to meet regulatory requirements.

Asia-Pacific – Fastest Adoption of 4K & Solar

China and South Korea lead in high-resolution camera volume, with Reolink and Hikvision introducing solar-powered PoE models for off-grid use.

7. Investment Outlook

Two opportunities stand out. First, the commercial small-business segment remains underserved: only 18% of U.S. small businesses have installed smart security cameras, versus 42% of households. Manufacturers that offer affordable multi-camera bundles with cloud-based remote monitoring can capture this gap. Second, the Matter protocol’s growing adoption will simplify cross-ecosystem integration, allowing a single app to control cameras, locks, and lights—lowering a key barrier for smart home novices. The most concrete risk is regulatory: state-level privacy laws (e.g., Illinois’ Biometric Information Privacy Act) impose strict consent requirements for facial recognition features. Non-compliance can lead to class-action lawsuits, as seen in recent suits against Ring. Companies must invest in compliance-by-design or risk expensive litigation.

Strategic Considerations:

- Matter Protocol Integration: Smart cameras that adopt Matter can interoperate with any smart home hub, reducing consumer indecision and expanding addressable market.

- Vertical SaaS for Small Businesses: Offer bundled camera + cloud storage + AI analytics (e.g., people counting) for retail stores, a high-margin niche with low competition.

- Biometric Privacy Lawsuits: Illinois BIPA litigation against Ring has set precedents; companies must obtain explicit opt-in for facial recognition or face class-action settlements up to $5,000 per violation.

- Chip Supply Volatility: Even with easing shortages, AI vision processors remain on long lead times; diversifying suppliers to include Chinese makers (e.g., Horizon Robotics) is critical.

Frequently Asked Questions

Make Informed Decisions in the Smart Security Camera Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-06-08. All market figures are estimates and may vary from actual results.